Medallion Financial Corp. Urges Shareholders to Vote for Its Highly Qualified Director Nominees Ahead of 2026 Annual Meeting

Company Highlights Record-Breaking Financial Performance as Successful Business Transformation has Created Historic Value for Shareholders

Exceptional Board Leadership and Oversight has Assured Effective Execution of the Strategic Plan

ZimCal’s Interest is Not Aligned with Common Shareholders’; ZimCal wants Medallion to Purchase its Trust Preferred Shares at a Premium to Market Value

ZimCal’s Self-Serving, Disruptive Third Consecutive Campaign Proposes Unqualified Nominees Who May Derail Company’s Current Growth Trajectory

NEW YORK, May 26, 2026 (GLOBE NEWSWIRE) -- Medallion Financial Corp. (NASDAQ: MFIN) (“Medallion” or the “Company”) today issued the following statement in connection with its 2026 Annual Meeting of Shareholders, urging shareholders to vote on the WHITE universal proxy card FOR the Company’s three highly qualified director nominees: John Everets, Cynthia A. Hallenbeck, and Alvin Murstein.

Background

Medallion’s historic run of shareholder value creation is under threat of disruption by a debt investor who vowed to wage proxy fights until the Company agrees to buy out his multimillion-dollar debt investment for a significant personal profit.

This campaign marks the third proxy contest launched in three years by ZimCal, a firm led by Stephen Hodges who purports to specialize in distressed credit and debt, yet refuses to disclose the total assets he manages. In 2021, Mr. Hodges acquired $15 million of trust preferred securities (TruPS) issued by Medallion Financing Trust I in 2007, which are highly illiquid instruments of subordinated debt.

At the time of his investment, the Company was undergoing a strategic transformation from primarily a taxi medallion lender to a specialty finance and consumer lending business. Despite the magnitude of the transformation, which has led to record profits and massive shareholder value creation, ZimCal has continued to pursue disruptive campaigns primarily because its holdings are predominantly debt not equity. Accordingly, ZimCal, in the absence of any common shares held over a significant time period, has not benefited from Medallion’s earnings accretion to the same extent as long-term shareholders.

In late 2023, the Company had discussions with Mr. Hodges and offered to acquire his TruPS at a reasonable price beneficial to all shareholders. Insistent on receiving a premium for his shares greatly in excess of fair value, Mr. Hodges launched his first campaign in 2024. He vowed that if Medallion did not grant him two Board seats, one for himself and another nominee at the time, and/or buyout his debt position for a profit between $5.25 and $6.5 million, he would wage a proxy contest every year until successful. The 2026 campaign is Mr. Hodges’ latest effort to follow through on his promise.

Medallion has Delivered the Best Results in its History

Medallion’s Board of Directors and management team have executed a remarkable transformation of the Company, and the results speak for themselves. The past five years represent the strongest period of financial performance in Medallion’s history.

Record Financial Performance Since IPO

- 2025 marked the best five-year period of financial performance in the Company’s history, with record highs in Net Interest Income and book value per share since Medallion’s initial public offering in 1996

- From 2021 through 2025, the Company doubled its core consumer loan portfolio to $2.5 billion, with Net Interest Income growing at a compound annual growth rate of 14.1%

- Net income generated over the last five years of $266 million ($378 million before tax) exceeds the combined net income of Medallion’s first 25 years as a public company

- Book value per share increased over 53% since fiscal year 2021, rising from $11.40 to $17.53

- Operating costs as a percentage of Net Interest Income was 39% during 2025, compared to 44% in 2021

Strong Total Shareholder Return

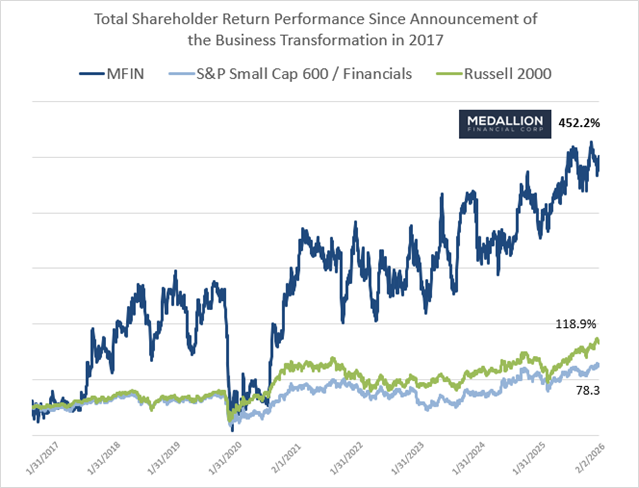

- The strategic transformation has generated a total shareholder return of 452% since the Company began shifting its primary focus to Medallion Bank and the consumer finance segment 1

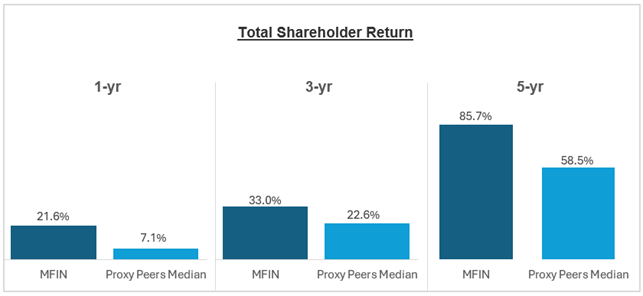

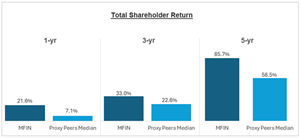

- Medallion’s Total Shareholder Return has significantly outperformed its proxy peer group across 1-, 3-, and 5-year periods, reflecting the strength of the Company’s strategic execution

- Since the 2024 Annual Meeting at which ZimCal’s nominees were defeated at a vote, shareholders have realized a total return of 35%2

Source: FactSet. Based on starting date Jan. 31, 2017 and ending date Feb. 2, 2026 (unaffected date, one day before ZimCal’s public letter dated February 3, 2026). Jan. 31, 2017 starting date based on Medallion’s press release regarding the transformation plan: https://www.medallion.com/pdf/news_press_releases/press_release_17-01-31.pdf

Source: FactSet. Based on Total Shareholder Return as of Feb. 2, 2026

Robust Capital Returns to Shareholders

- Since 2022, the Company has returned more than $68.5 million to shareholders through dividends and share repurchases

- The quarterly dividend has been raised consistently, and the current dividend of $0.14 per share represents a 75% increase from the $0.08 per share quarterly dividend paid in fiscal year 2022

- A $75 million notes offering led by JP Morgan Investment Management Inc.3, reaffirmed market confidence in Medallion’s Board and management, receiving an investment-grade A– rating from Egan-Jones

- Independent analyst currently have favorable ratings on Medallion stock, with a BUY rating issued by Ladenburg Thalmann and MARKET PERFORM issued by Northland Capital Markets

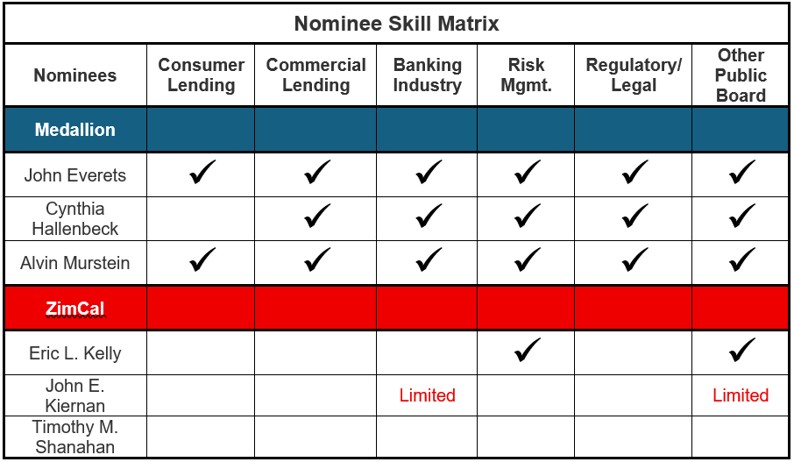

Medallion’s Board is Responsible for Value Creation. It has the Relevant Experience, Skills, and Track Record to Sustain Existing Momentum

The transformation Medallion has achieved did not happen by accident. It was driven by a Board purposefully constructed with the right mix of expertise in consumer lending, commercial banking, financial management, risk oversight, and corporate governance. The nominees standing for election at the 2026 Annual Meeting were central to this transformation and are the right directors to oversee the Company’s continued growth.

John Everets — Independent Director

- Brings decades of executive leadership in banking and financial services

- As former Chairman and CEO of the Bank of Maine, led a successful recapitalization and turnaround of a financially stressed institution, ultimately positioning the entity for a $135 million sale to Camden National Corporation

- Served on the Medallion Bank Board since 2019, providing hands-on oversight of the company’s lending and financial strategy

- Expertise spans consumer lending, commercial lending, banking industry operations, risk management, regulatory and legal affairs, and public company governance

Cynthia A. Hallenbeck — Independent Director

- Has over 30 years of financial management experience, including her role as CFO of Citigroup’s treasury department and prior service as a director of Walker & Dunlop

- Deep expertise in commercial lending, banking, risk management, regulatory affairs, finance and accounting, and public company governance makes her a critical voice on Medallion’s Board

Alvin Murstein — Executive Chairman

- Architect of Medallion’s storied history and its successful transformation

- Led the Company’s strategic pivot from taxi medallion lending to a thriving consumer lending business

- With over 60 years of experience in ownership, management, and specialty finance, and an approximately 7.99% ownership stake, Mr. Murstein’s interests are deeply aligned with those of all shareholders

Together, these three nominees hold deep and complementary expertise across every dimension critical to Medallion’s continued success, expertise that ZimCal’s nominees simply cannot match.

ZimCal has No Plan, Misaligned Interests, and Unqualified Nominees

For the third consecutive year, ZimCal has launched a disruptive would-be activist campaign against Medallion. In 2024, the Company’s nominees received 3.5 times as many votes as Mr. Hodges and his co-nominee received. In 2025, following ZimCal’s campaign withdrawal, each of the Board’s nominees was elected with at least six times the favorable votes over withholds, with Andrew Murstein, the Company’s current CEO, receiving nearly 95% approval from shareholders. Shareholders saw through these false campaign narratives of Mr. Hodges before, and the Board believes he will do so again.

ZimCal’s Interests Are Not Aligned with Shareholders

ZimCal is first and foremost a debt investor, not a long-term equity owner. Its illiquid position in preferred securities of Medallion Financing Trust I matures in September 2037. The Company believes the primary motivation is to pressure Medallion into repurchasing this illiquid position at a significant premium to its current value. In his February 2024 ultimatum, Mr. Hodges explicitly demanded that Medallion purchase his debt, under structures that would have generated an estimated $5.25 million to $6.5 million in profit for him at the expense of shareholders.

Further underscoring its short-term, opportunistic intent: ZimCal held only an estimated 3,000 shares as recently as March 2026 and has accumulated the vast majority of its current equity stake in recent weeks. This timing suggests an effort to influence the outcome of this year’s Annual Meeting by falsely claiming that he is aligned with investors, not to build long-term value alongside fellow shareholders. We suspect, just like he’s done in the past, Mr. Hodges will dispose of his recently acquired shares after the June 9th shareholders’ meeting.

We urge shareholders to be wary of ZimCal’s abrupt effort to acquire shares just prior to the Annual Meeting vote, as such an investor is NOT aligned with your long-term interests.

ZimCal Has a Flawed Understanding of Our Business

ZimCal has consistently demonstrated a fundamental misunderstanding of Medallion’s business, its accounting, and its growth strategy. Its criticisms have repeatedly been proven wrong: concerns about dividends proved to be false, concerns about credit quality proved to be exaggerated, and concerns about financial performance were contradicted by record results. The Board believes that acting on ZimCal’s unfocused and uninformed agenda would risk derailing the very momentum that has made Medallion the success story it is today.

Market Analysts Do NOT Share ZimCal’s Negative View of Medallion’s Performance

Analysts covering Medallion each reflect a favorable view of the Company’s recent performance and future outlook:

“…we viewed 2026 as a year of investing in the business to set up MFIN for a robust 2027 and 2028…”

“Underneath the headline, the core franchise performed inline, with net interest income growth, modest NIM expansion, and continued loan book growth as MFIN pivots away from its legacy taxi lending business.”

“MFIN reported further improvement in net interest margin on both gross and net loans, which is promising. Overall, originations and the portfolio size are reflecting strength in the platform and consistent execution across the company's business lines.”

– Northland Capital Markets, Research Report April 30, 2026

“We view 1Q26 results as an aberration to the attractive total return profile MFIN has produced over the past several quarters, and we expect earnings will improve....”

– Ladenburg Thalmann, Research Report April 30, 2026

ZimCal has a history of raising misleading and unfounded concerns about Medallion’s business and financial position:

- In 2024, ZimCal warned of “rapid deterioration” in key operating metrics, yet since the 2024 Annual Meeting, Medallion has delivered a total shareholder return of approximately 35%, achieved its highest net interest income in five years and expanded net interest margin in FY2025.

- In 2025, ZimCal claimed Medallion may struggle to pay dividends and operating expenses. In reality, Medallion increased its quarterly dividend in both FY2025 and year-to-date 2026. The current 2Q2026 dividend is 75% higher than its FY2022 quarterly dividend.

- ZimCal now points to quarterly net income while ignoring the impact of non-recurring equity investment gains and the fact that net interest income after provision for credit losses grew year-over-year in 1Q2026.

- ZimCal’s current attacks on charge-offs and Strategic Partnerships again omit basic context: Medallion’s loan book has grown materially, consumer charge-offs are rising across the broader market, Strategic Partnership loans are held for only short periods and the program represented just $11 million of the total loan portfolio as of 1Q2026.

ZimCal Has No Credible Plan for Value Creation

ZimCal’s "plan” contains a vast array of ideas that are relevant to the banking sector more broadly, but very few are applicable or implementable to a company of Medallion’s size and resources. In addition, soundbites such as “Focus on Technology” and “Diversify Revenues” completely disregard the advances we have made in these areas toward shareholder value creation.

Regarding “Technology” and as previously noted, related investments paired with cost efficiencies have resulted in operating costs as a percentage of Net Interest Income declining to 39% in FY2025, compared to 50% in FY2020. Additionally, please note the following advances:

- 2022: Hired a new team lead to accelerate software engineering activity

- 2024: Hired VP of Data Analytics and expanded the data science team

- 2024: Migrated all new loans to a new loan servicing system

- 2025: Hired VP of Credit to strengthen model use and credit policy implementation

- 2026: Established business process re-engineering team

As far as “Diversifying Revenues,” ZimCal has not only failed to acknowledge the success of the business transformation to specialty finance, but also has made statements that conflict with reality as well as market sentiments concerning certain diversification programs already implemented.

For example, ZimCal’s claims that the Strategic Partnership Program is “poorly allocated” and “losing money” demonstrates a poor understanding of this business. Strategic Partnership business requires minimal capital commitment due to the small size of average loans provided and the short holding periods (less than 5 days). As disclosed in the 2025 10-K, the loans or receivables originated are held for up to three business days only. In 2025, Medallion originated $771.6 million of strategic partnership loans and held $15.1 million as of December 31, 2025. The average yield on these loans was 15.7% with total fee and interest income of $6.5 million. The program allows Medallion to build relationships with fintech companies and generate additional fee income without significantly leveraging the balance sheet.

In Northland Capital Markets’ most recent report update, the analyst notes:

“…strategic partnership program continuing to scale into a meaningful growth engine…”

Accordingly, ZimCal’s recommendation to end the Strategic Partnerships program along with many other misrepresentations, highlights a lack of understanding of our business. ZimCal’s ideas, we believe, would jeopardize the success and growth we have achieved in recent years.

ZimCal’s Nominees Lack the Relevant Skills and Experience

The Medallion Nominating and Governance Committee conducted a thorough review, including individual interviews, of ZimCal’s three nominees. It concluded that their backgrounds and skillsets are NOT additive to the Board. None of ZimCal’s nominees has direct experience operating a consumer lending platform comparable to Medallion’s. A review of their skillsets reveals critical gaps across consumer lending, commercial lending, banking industry expertise, and risk management, which are among the very competencies most essential to overseeing Medallion’s growth strategy. In contrast, each of Medallion’s nominees brings a comprehensive skill set directly applicable to the Company’s business and governance needs.

ZimCal nominee, Eric Kelly, lacks relevant experience and has destroyed shareholder value

- Eric Kelly’s background is primarily in enterprise storage and hardware technology, and not specialty finance or consumer lending.

- He served as the CEO of Sphere 3D from 2014 to 2018. During his tenure, Sphere 3D’s market value fell by 99%4.

- More recently, Mr. Kelly joined the board of Sabre Corporation effective Jan. 1, 2025. Sabre’s total shareholder return is negative (55%) since his appointment5.

Medallion’s shareholders deserve a board that has a history of creating shareholder value not one with a track record of shareholder value destruction.

ZimCal nominee John Kiernan’s turnaround experience at Alico – a holding company focused on agricultural operations – has no relevance to Medallion’s consumer and commercial lending operations

- John Kiernan has served as the President, CEO, and previously CFO, of Alico for the past 11 years. According to the company’s website, Alico is “a holding company with assets and related operations in agriculture and environmental resources, including citrus and wildlife management.” Clearly, this business has very little in common with Medallion.

- Mr. Kiernan’s limited experience at PeoplesBank was due to a settlement agreement between Codorus Valley Bancorp, the parent company of PeoplesBank, and Driver Management (a hedge fund) in Feb. 20226. Codorus appointed Mr. Kiernan to its board effective April 12, 2022 – he was not recruited by PeoplesBank as part of a director search process. In fact, he did not continue to serve as a director after the merger between Orrstown Bank and PeoplesBank7.

- Outside of a two-year stint at PeoplesBank and a seven-month stay at Susquehanna International Group, Mr. Kiernan’s banking experience is mostly comprised of his 10+ year tenure at Bear Stearns which ended just prior to the bank’s collapse.

ZimCal nominee Timothy Shanahan’s experience as a proclaimed turnaround/ restructuring specialist is not a skillset the Board currently seeks nor is aligned with Medallion’s strategy

- Mr. Shanahan has no direct experience operating a consumer lending platform.

- His expertise in distressed, turnaround, and restructuring situations has little relevance to Medallion as our business transformation has largely been completed.

- He has no prior public board experience.

The Choice is Clear: Medallion’s Board and Management have a Proven Track Record

Medallion’s Board and management team have executed a remarkable transformation of the Company, and the results speak for themselves. The past five years represent the strongest period of financial performance in Medallion’s history.

The Board urges shareholders to reject ZimCal’s self-serving campaign and instead support the directors who have actually built, and are continuing to build, value for all shareholders.

Medallion reminds shareholders that every vote is important and encourages shareholders to vote TODAY on the WHITE universal proxy card “FOR” ONLY the Board’s nominees, Mr. Everets, Ms. Hallenbeck, and Mr. Murstein, and “FOR” the approval of the 2026 compensation paid to our named executive officers.

The Board urges Medallion stockholders to DISCARD all blue proxy cards and materials sent by Mr. Hodges.

Stockholders who have any questions or need assistance voting may call our proxy solicitors, Alliance Advisors, toll-free at (844) 202-5720.

Medallion’s definitive proxy statement and other materials regarding the Board of Directors recommendations for the 2026 Annual Meeting can be found at www.votemedallion.com/.

About Medallion Financial Corp.

Medallion Financial Corp. (NASDAQ: MFIN) and its subsidiaries originate and service a portfolio of consumer loans and mezzanine loans in various industries. Key industries served include recreation (towable RVs and marine) and home improvement (replacement roofs, swimming pools, and windows). Medallion Financial Corp. is headquartered in New York City, NY, and its largest subsidiary, Medallion Bank, is headquartered in Salt Lake City, Utah. For more information, please visit www.medallion.com.

Forward-Looking Statements

Please note that this press release contains forward-looking statements that involve risks and uncertainties relating to business performance, cash flow, net interest income and expenses, other expenses, earnings, growth, and our growth strategy. These statements are often, but not always, made using words or phrases such as “will” and “continue” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These statements relate to future public announcements of our earnings, expectations regarding our loan portfolio, including collections on our taxi medallion loans, the potential for future asset growth, and market share opportunities. Medallion’s actual results may differ significantly from the results discussed in such forward-looking statements. For example, statements about the effects of the current economy, whether inflation or the risk of recession, the effects of tariffs, the impact of the conflict with Iran, operations, financial performance and prospects constitute forward-looking statements and are subject to the risk that the actual impacts may differ, possibly materially, from what is reflected in those forward-looking statements due to factors and future developments that are uncertain, unpredictable and in many cases beyond Medallion’s control. In addition to risks relating to the current economy, for a description of certain risks to which Medallion is or may be subject, please refer to the factors discussed under the heading “Risk Factors” in Medallion’s 2025 Annual Report on Form 10-K.

Important Additional Information and Where to Find It

Medallion has filed its definitive proxy statement, accompanying WHITE universal proxy card and other relevant documents with the Securities and Exchange Commission (“SEC”) in connection with the solicitation of proxies for Medallion’s upcoming 2026 Annual Meeting of Shareholders. BEFORE MAKING ANY VOTING DECISION, SHAREHOLDERS OF THE COMPANY ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH OR FURNISHED TO THE SEC, INCLUDING MEDALLION’S DEFINITIVE PROXY STATEMENT AND ANY AMENDMENTS AND SUPPLEMENTS THERETO, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and shareholders will be able to obtain a copy of the definitive proxy statement and other documents filed by the Company with the SEC free of charge from the SEC’s website at www.sec.gov. In addition, copies will be available at no charge by visiting the “Investor Relations” section of Medallion’s website at www.medallion.com, as soon as reasonably practicable after such materials are filed with, or furnished to, the SEC.

Investor Relations

InvestorRelations@medallion.com

212-328-2176

Investor Relations

The Equity Group Inc.

Lena Cati

lcati@theequitygroup.com

(212) 836-9611

Val Ferraro

vferraro@theequitygroup.com

(212) 836-9633

1 Total shareholder return calculated using starting date of Jan. 31, 2017 and ending date of Feb. 2, 2026. The starting date is based on Medallion’s press release regarding the transformation plan: https://www.medallion.com/pdf/news_press_releases/press_release_17-01-31.pdf

2 Total shareholder return calculated using starting date of June 11, 2024 and ending date of Feb. 2, 2026.

3 Source https://www.globenewswire.com/news-release/2026/04/28/3283166/0/en/medallion-financial-corp-announces-completion-of-private-placement-of-75-0-million-of-senior-notes-to-group-led-by-jp-morgan-investment-management-inc.html

4 Source: FactSet. Data from Dec. 1, 2014 to Nov. 18, 2018

5 Source: FactSet. Data from Jan. 1, 2025 to May 15, 2026

6 https://www.businesswire.com/news/home/20220202005558/en/Driver-Management-Nominates-Three-Highly-Qualified-Independent-Candidates-for-Election-to-Codorus-Valley-Bancorps-Board-of-Directors

7 https://content-archive.fast-edgar.com/20240701/AI2Z3G2CZW22FZI222282Z425WO9ZC22D262/ef20031916_ex99-1.htm

Images accompanying this announcement are available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/50beda21-3336-4d84-aec7-c135a47338d4

https://www.globenewswire.com/NewsRoom/AttachmentNg/3ad8a3f1-b7c5-447e-915e-cba8e48bf9de

https://www.globenewswire.com/NewsRoom/AttachmentNg/7d69f65f-5065-41d7-8cd1-96c2b711ebb0

![]()

Total Shareholder Return Performance Since Announcement of the Business Transformation in 2017

Source: FactSet. Based on starting date Jan. 31, 2017 and ending date Feb. 2, 2026 (unaffected date, one day before ZimCal’s public letter dated February 3, 2026). Jan. 31, 2017 starting date based on Medallion’s press release regarding the transformation plan: https://www.medallion.com/pdf/news_press_releases/press_release_17-01-31.pdf

Total Shareholder Return

Source: FactSet. Based on Total Shareholder Return as of Feb. 2, 2026

Nominee Skill Matrix

Nominee Skill Matrix

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.